Taking payments is the key to any business and there are plenty of tools for taking money online. But when you look at the world of mobile commerce, a broad and baffling vista of ways that mobile can be used to pay and indeed to take payment, opens up.

So let’s take a look at the kinds of mobile payment tools that are available then, in the next few articles, look at some of the key proponents of these different ways of making mobile, cards, websites and money all work together.

Just a quick note, however, before we do that: there is a burgeoning world of mobile payments with many companies looking for an in. Here we look at just some of our favourites.

There, of course, many, many more… And remember that there are just ways of handling the transaction through mobile, you will still – with the exception of PayPal – need a payment platform and gateway to connect this to your merchant bank account to actually get the money.

So what types of m-payments tech is there?

Card readers

The obvious place to start with taking money via mobile is in turning the phone or tablet into a card reader using either plug in devices such as Square, or using software that lets you photograph the card such as ScanPay, or just lets you key in the number (all the others!).

Square: turns a smartphone into a mobile PoS

ScanPay: simply photograph the card to make a payment

These tools are ideal for tradesmen such as plumbers and odd job men, but increasingly they are gaining traction with independent retailers and even bigger chains, as they look to revolutionise how in store payments are taken. Of course, for the online only business they can also be used to take payments over the phone.

Then there is the sticky world of NFC. This is clearly aimed at the more high-end retailer, but worth including here nonetheless as it is starting to gain some traction and eventually it will scale down to the small end.

This is a physical paying mechanism whereby the user taps their NFC enabled device against an NFC reader at the POS. To date, we have seem limited trials of NFC cards in Pret a Manger, but we are yet to see a widespread roll out.

However, Transport for London is set to replace Oyster cards with contactless payment readers that take the payment as you make the journey so its coming.

Banking and card apps

The other place to turn to start taking mobile payments is through apps from the bank or from card companies. The best known is Barclay’s Pingit, which allows consumers to pay bills and order things on line using the Barclay’s Pingit app. This is set to also be rolled out to allow for payments in shops.

It started as a peer-to-peer (p2p) payment tool, which makes it in some ways ideally scaled for SMEs (see p2p Payments below), and it looks to have great potential.

Barclay’s PingIt: “Payment as easy as sending a text”

Similarly, Visa and MasterCard have both rolled out their own payment apps that allow for card payments either online or via the phone in store and these, given that they are from trusted brands, are likely to take off pretty quickly once out of the trial stage.

MasterCard’s Qkr! is gaining traction in restaurants and other retailers with physical stores as it prints out a code on the receipt that customer taps into the app to pay that retailer.

Qtr!: gaining ground in restaurants

Payment APIs

While banks and card companies have developed apps and mobile services to ease mobile payments, a raft of third party payment apps have grown up in the market too. In 2015 there were literally hundreds: today there are far fewer, with most having bitten the dust. Why? They arrived too early for consumer buy in and because they have been squashed by those apps from more powerful suppliers.

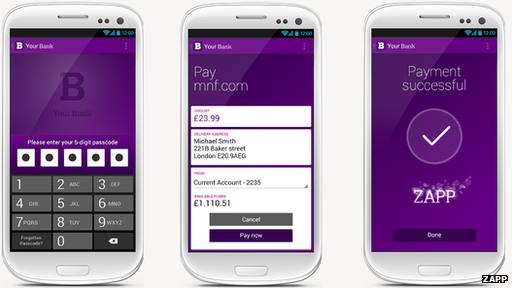

There are, however, still too many to mention here individually, but the main ones – Zapp (trading these days as PayByBankApp – way less snappy!), Judo, Braintree and its parent Paypal – all offer the chance to add simple mobile payments to your website or into your store by just adding a few lines of code to your sire and offer a seamless, secure way for consumers to pay.

Each of these services (unlike Wallets, below) don’t require any account creating, instead linking a bank account to a mobile phone number or, in the case of Paypal, a card to an account that works online or on a phone.

These apps offer a simple way to add m-payments but they do come at a price to the merchant, often being slighting to very much more expensive than card payments.

Judo: Just add a few lines of code to take mobile payments

Wallets

Mobile wallets differ from payment apps – in my ad hoc definition at least – in that they are just a way to hold a card or cards (and even these days coupons and loyalty points) and then use the phone’s inbuilt functionality to allow for payments to be made. These can be in physical stores or online and are in many ways the most simple way to ‘do’ mobile payments.

The most notable are of course Apple Pay and Android Pay, although others have tried. There are wallet apps for consumers from banks, and even O2 and Vodafone have tried. From the retailers point of view, it doesn’t matter how many wallet APIs there are, you just have to accept payments from phones.

The advantage with the likes of Apple Pay is that it is relatively easy to connect the card to the phone and then very easy to make payments online or in store – where there is contactless payment terminals and you are spending less than £30 – as it requires just a touch of the finger print ID button.

Apple Pay: Touch ID makes it quick, easy and secure

Accounts and third parties

Akin to wallets are third party accounts and payment services where the user essentially sets up an account and gives all their payment details once or keeps an account topped up.

Topped up accounts are slowly losing favour as, frankly, they are a pain to keep up to date and other payment tools have superseded them. However, third party payment tools where the user signs up and then can use that stored card are becoming increasingly popular across many mainstream retailer sites.

If you want to add this to your site then look no further than PayPal or Payments by Amazon.

Using the phone itself

One of the much overlooked ways of using mobile for payments is using the phone bill.

These premium rate services are often associated with adult services and the like, but increasingly through an initiative called Payforit, payment service providers can now offer the ability to pay through mobile and for the cost of the purchase to be put on the phone bill.

Payforit: use your phone bill to pay for things

So far this only works for digital and non-real world goods such as in-app purchases, buying wifi on trains and carparking, but it could soon offer small independent merchants a nice way to take simple and quick low value ‘micro payments’ once the rules are changed. Definitely one to watch.

p2p money transfer services

There is also a growing move towards peer-to-peer money transfer services on mobile, that allow ordinary people to tie their mobile number to a bank account and to then pay other people who have done the same simply using a text message.

These services – most recently and effectively exemplified by Paym (pronounced Pay em) – are designed to let people “pay that tenner I owe you for the taxi on Friday” or “here’s my half of the chinese we had yesterday”, but they are interesting, I believe, to SMEs as they can be used to pay for things.

As with most things m-payments related it is early days and there are no p2p mobile payment tools targeted at SMEs, but their time will come.